ID : MRU_ 429946 | Date : Nov, 2025 | Pages : 258 | Region : Global | Publisher : MRU

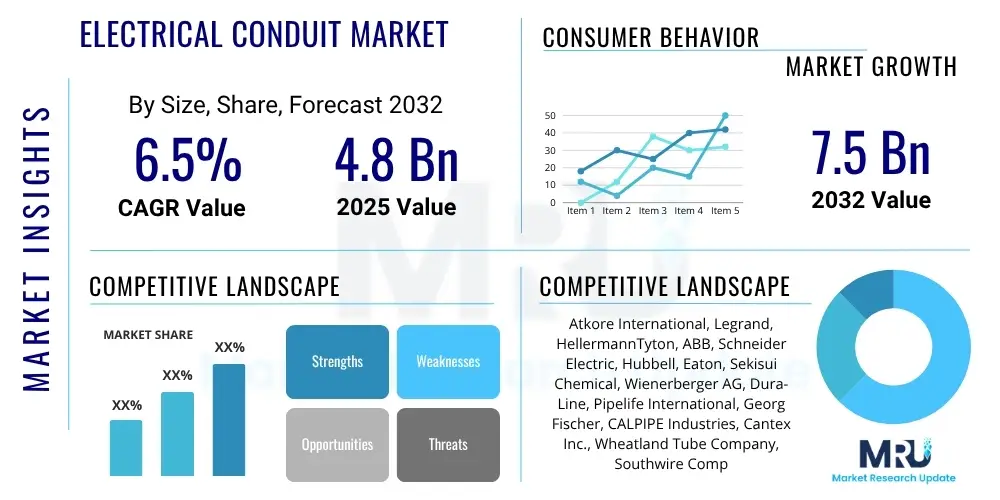

The Electrical Conduit Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2032. The market is estimated at $4.8 Billion in 2025 and is projected to reach $7.5 Billion by the end of the forecast period in 2032.

The electrical conduit market encompasses the manufacturing, distribution, and application of tubular protective systems used to house and safeguard electrical wires and cables in various installations. These conduits provide crucial mechanical protection against physical damage and environmental factors such as moisture, chemicals, and extreme temperatures. They also play a vital role in ensuring electrical safety by preventing short circuits, fires, and electric shocks, while also facilitating future wiring changes or upgrades.

The product range within this market is diverse, including materials like rigid metallic conduit (RMC), intermediate metallic conduit (IMC), electrical metallic tubing (EMT), rigid PVC conduit, flexible metallic conduit (FMC), liquid-tight flexible metallic conduit (LFMC), and fiberglass conduit. Each type is designed for specific environmental conditions and application requirements, from heavy-duty industrial settings to residential and commercial buildings. Major applications span across residential construction, commercial complexes, industrial facilities, data centers, and public infrastructure projects such as bridges and tunnels, where robust and reliable electrical containment is paramount.

The primary benefits of electrical conduits include enhanced safety, extended wire lifespan, simplified wiring maintenance, and compliance with strict electrical codes and standards. Driving factors for market growth are strongly linked to global infrastructure development, rapid urbanization, increasing industrialization, and a heightened focus on electrical safety regulations worldwide. The continuous demand for new construction, coupled with renovation and upgrading activities in existing structures, consistently fuels the expansion of the electrical conduit market, making it an essential component of the global electrical ecosystem.

The Electrical Conduit Market is experiencing dynamic shifts driven by evolving construction practices, technological advancements, and a growing emphasis on safety and efficiency. Business trends indicate a strong move towards pre-fabricated conduit systems, which reduce installation time and labor costs on construction sites, thereby boosting project efficiency. Additionally, there is an increasing demand for sustainable and fire-retardant materials, reflecting heightened environmental awareness and stricter safety regulations across the globe. Digitalization in construction, including Building Information Modeling (BIM), is also influencing how conduits are planned and integrated, leading to more optimized and waste-reduced installations.

Regionally, the Asia Pacific continues to emerge as the dominant and fastest-growing market, propelled by massive infrastructure projects, rapid urbanization, and industrial expansion in countries like China, India, and Southeast Asian nations. North America and Europe, while mature markets, demonstrate steady growth fueled by significant investments in smart city initiatives, renewable energy projects, and ongoing renovation and retrofitting activities. The Middle East and Africa, along with Latin America, show promising potential with nascent but expanding construction sectors and increasing foreign investments in infrastructure development, driving demand for electrical conduit solutions.

Segmentation trends highlight the continued dominance of non-metallic conduits, particularly PVC, due to their cost-effectiveness, corrosion resistance, and ease of installation. However, metallic conduits maintain a critical role in high-stress industrial environments where superior mechanical protection and electromagnetic shielding are required. Flexible conduits are seeing increased adoption in complex installations and renovation projects where adaptability is key. The market is further segmented by end-use, with commercial and industrial sectors representing the largest consumers, driven by the need for robust and code-compliant electrical systems to support complex machinery and extensive data networks.

User inquiries regarding AI's influence on the electrical conduit market primarily revolve around optimizing manufacturing processes, enhancing supply chain efficiency, enabling predictive maintenance for installations, and integrating smart functionalities into conduit systems. Key themes highlight expectations for AI to automate quality control, forecast material demand accurately, and contribute to safer, more efficient electrical infrastructures. There is significant interest in how AI can move conduits beyond passive protection to active monitoring components within smart buildings, addressing concerns about system uptime and operational costs.

The electrical conduit market is shaped by a confluence of drivers, restraints, opportunities, and external impact forces that dictate its growth trajectory and competitive landscape. Key drivers include accelerating global infrastructure development, particularly in emerging economies, which necessitates extensive electrical wiring and protective solutions. Rapid urbanization and industrialization further fuel demand for robust electrical systems in new residential, commercial, and industrial facilities. Furthermore, the stringent adherence to electrical safety codes and building regulations worldwide mandates the use of conduits to prevent hazards and ensure compliance, thereby consistently driving market expansion.

Conversely, the market faces several restraints. Volatility in raw material prices, such as steel and PVC resin, can significantly impact manufacturing costs and profit margins, leading to pricing pressures. Intense competition among manufacturers, both global and local, can also suppress prices and reduce profitability. Additionally, a shortage of skilled labor for installation and maintenance of complex electrical systems, especially in niche conduit applications, poses a challenge. Environmental concerns related to the production and disposal of certain conduit materials, particularly plastics, also present a restraint, pushing for more sustainable alternatives.

Opportunities abound for market participants willing to innovate and adapt. The growing trend towards smart building technologies and integrated automation systems offers a pathway for developing "smart conduits" equipped with sensors for monitoring and data transmission. The increasing adoption of modular and pre-fabricated construction techniques can streamline conduit installation processes, opening new avenues for specialized product offerings. Moreover, the push for sustainable and green building practices is creating demand for eco-friendly conduit materials and production methods. Emerging economies, with their vast unmet infrastructure needs, represent significant untapped potential for market growth.

Impact forces such as global economic growth directly influence construction spending, which is a primary determinant of conduit demand. Changes in regulatory landscapes, including updated electrical codes and environmental policies, force manufacturers to innovate and ensure compliance. Technological advancements in material science and manufacturing processes enable the development of lighter, stronger, and more durable conduits. Finally, growing environmental awareness among consumers and policymakers is steering the market towards more sustainable and recyclable conduit solutions, impacting material choices and product development strategies.

The Electrical Conduit Market is broadly segmented based on various critical parameters including the material used for manufacturing, the type or flexibility of the conduit, the specific application areas, and the end-use industry utilizing these products. This comprehensive segmentation helps in understanding the diverse needs of different sectors and regions, allowing manufacturers to tailor their product offerings and marketing strategies effectively. Each segment reflects unique characteristics, performance requirements, and cost considerations, contributing to the overall complexity and dynamism of the market landscape. Analyzing these segments provides a clear picture of market penetration, growth potential, and competitive dynamics across different product categories and applications.

The value chain for the electrical conduit market begins with the upstream segment, primarily involving the sourcing and processing of raw materials. This includes steel manufacturers supplying galvanized steel for metallic conduits, petrochemical companies providing PVC resins and HDPE for non-metallic conduits, and aluminum producers. These raw material suppliers form the foundational layer, dictating the quality, cost, and availability of primary components. Efficient procurement and stable supply relationships with these upstream partners are crucial for manufacturers to maintain competitive pricing and consistent production schedules.

Moving downstream, the value chain progresses through the manufacturing processes where raw materials are transformed into various types of electrical conduits through extrusion, molding, galvanization, and other fabrication techniques. Manufacturers, often large-scale enterprises, then distribute their products through a complex network. This distribution channel typically involves a combination of direct sales to large construction projects or industrial clients, and indirect sales through a network of wholesalers, distributors, and retailers. Wholesalers and distributors play a pivotal role in reaching a broad customer base, managing inventory, and providing logistics support, especially for smaller contractors and regional projects.

The final segment of the value chain involves the end-users, which include electrical contractors, construction companies, industrial facilities, and various infrastructure developers who install the conduits. After installation, ongoing maintenance and potential upgrades continue to contribute to the market's activity. The distinction between direct and indirect distribution is significant; direct channels offer manufacturers greater control over sales and customer relationships, particularly for customized or high-volume orders, while indirect channels provide wider market reach, leveraging the established networks and specialized services of intermediaries to cater to diverse and geographically dispersed customer segments.

Potential customers for electrical conduit products encompass a broad spectrum of industries and project types, all requiring safe, compliant, and durable enclosures for electrical wiring. The primary end-users are entities involved in construction and infrastructure development across residential, commercial, and industrial sectors. This includes large-scale general contractors responsible for entire building projects, as well as specialized electrical contractors who perform the wiring and conduit installation tasks. Their demand is driven by new construction, renovation, and maintenance needs, requiring conduits for everything from basic lighting circuits to complex power distribution systems.

Beyond traditional construction, industrial facilities, such as manufacturing plants, chemical processing units, and power generation stations, represent significant buyers. These environments often demand specialized conduits that can withstand harsh conditions, including corrosive chemicals, extreme temperatures, and heavy mechanical stress, ensuring the uninterrupted operation of critical machinery. Data centers and telecommunications companies also constitute a growing customer base, relying on conduits for protecting sensitive data and communication cables, often requiring solutions that offer excellent electromagnetic interference shielding and fire resistance to ensure data integrity and network uptime.

Furthermore, government agencies and public works departments are key customers for infrastructure projects like bridges, tunnels, roads, and public utility installations (water treatment plants, power grids). These projects require robust, long-lasting conduit systems capable of enduring outdoor elements and heavy-duty use over decades. Real estate developers, who oversee the construction of residential communities, commercial complexes, and mixed-use properties, also consistently purchase conduits as fundamental components of their electrical systems. The diverse needs of these end-users emphasize the market's need for a wide range of conduit materials, types, and sizes, tailored to specific application demands and regulatory compliance.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | $4.8 Billion |

| Market Forecast in 2032 | $7.5 Billion |

| Growth Rate | 6.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Atkore International, Legrand, HellermannTyton, ABB, Schneider Electric, Hubbell, Eaton, Sekisui Chemical, Wienerberger AG, Dura-Line, Pipelife International, Georg Fischer, CALPIPE Industries, Cantex Inc., Wheatland Tube Company, Southwire Company, Wesco International, Zekelman Industries, NIBCO Inc., Argos USA |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The electrical conduit market is increasingly influenced by advancements in materials science, manufacturing processes, and digital integration, driving innovation beyond traditional wire protection. A significant technological trend is the development of advanced materials that offer superior performance characteristics, such as enhanced fire resistance, improved corrosion protection, and lighter weight without compromising mechanical strength. This includes specialized coatings for metallic conduits and advanced polymer blends for non-metallic conduits, enabling their use in more demanding environments and contributing to extended product lifespans and reduced maintenance. The focus is also on materials that are more sustainable, recyclable, and have lower environmental footprints, aligning with global green building initiatives and circular economy principles.

Manufacturing technologies are evolving to improve efficiency, precision, and customization. Automation in extrusion and fabrication processes allows for higher production volumes, tighter tolerances, and consistent product quality. The adoption of pre-fabrication techniques is transforming on-site installation, with conduits being cut, bent, and assembled into modular units off-site, leading to faster, safer, and more accurate installations. This approach minimizes waste and labor costs at the construction site, supporting the broader trend of industrializing construction. Digital tools like Building Information Modeling (BIM) are integral here, enabling precise planning and coordination of conduit pathways within a virtual 3D model before physical construction begins.

Emerging technologies also include the integration of "smart" functionalities into conduit systems. While traditional conduits are passive, a new generation is being explored with embedded sensors capable of monitoring various parameters such as temperature, humidity, and even detecting wire faults or physical damage within the conduit itself. These smart conduits can communicate data to central building management systems, enabling predictive maintenance, optimizing energy usage, and enhancing overall electrical safety and system reliability. This technological shift positions conduits not just as protective enclosures but as active components within intelligent building infrastructures, offering real-time insights and contributing to more responsive and efficient electrical networks.

An electrical conduit is a durable tube or pipe used to protect and route electrical wiring in buildings and structures. Its importance lies in providing mechanical protection to wires from physical damage, moisture, and chemicals, ensuring electrical safety by preventing short circuits and fires, and facilitating future wiring changes or upgrades.

Electrical conduits are primarily categorized into metallic and non-metallic types. Metallic conduits include galvanized rigid conduit (GRC), intermediate metallic conduit (IMC), and electrical metallic tubing (EMT). Non-metallic conduits typically consist of PVC (Polyvinyl Chloride), HDPE (High-Density Polyethylene), and fiberglass. They also vary by flexibility, being either rigid or flexible.

Safety regulations significantly influence the electrical conduit market by mandating specific types of conduits for different applications to prevent electrical hazards. Compliance with codes like the National Electrical Code (NEC) or equivalent international standards drives demand for certified products, encourages material innovation for enhanced fire resistance and durability, and ensures the continuous adoption of conduits as an essential safety component in all electrical installations.

Key drivers for the electrical conduit market growth include rapid global urbanization and industrialization, leading to increased construction activities across residential, commercial, and industrial sectors. Additionally, significant investments in infrastructure development, rising awareness of electrical safety, and the continuous need for upgrading and renovating existing electrical systems are pivotal factors fueling market expansion.

The Asia Pacific (APAC) region currently dominates the electrical conduit market. This dominance is attributed to extensive infrastructure development projects, rapid urbanization, and industrial growth in countries such as China, India, and other Southeast Asian nations, leading to a high demand for electrical protective solutions in new constructions and expansions.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.