ID : MRU_ 432794 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

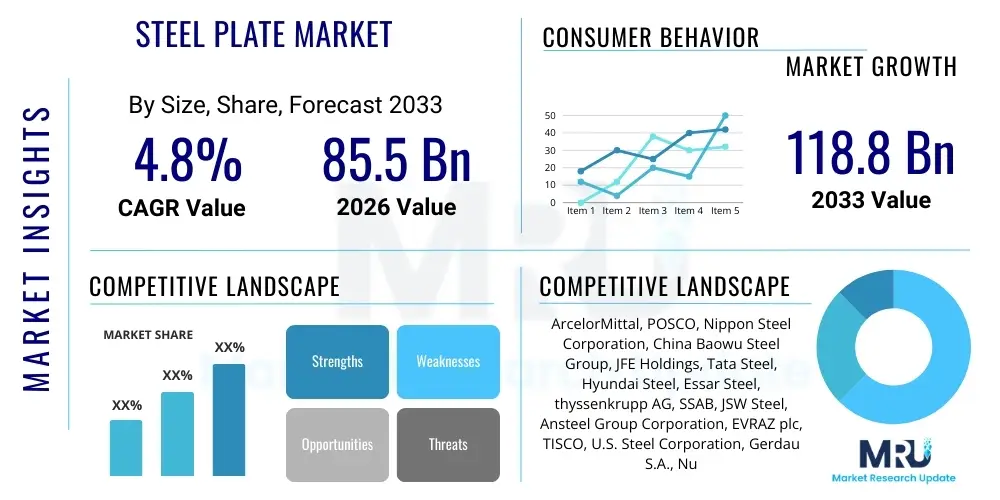

The Steel Plate Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2026 and 2033. The market is estimated at USD 85.5 Billion in 2026 and is projected to reach USD 118.8 Billion by the end of the forecast period in 2033. This growth trajectory is fundamentally driven by robust demand from high-volume, heavy industries globally, particularly infrastructure development, shipbuilding, and the burgeoning renewable energy sector.

The Steel Plate Market encompasses the production, distribution, and utilization of flat, rolled steel products characterized by a thickness greater than 6mm. These versatile products, often categorized by type such as carbon steel plate, alloy steel plate, and stainless steel plate, form the backbone of heavy construction and manufacturing globally. Steel plates offer unparalleled structural integrity, high tensile strength, and excellent weldability, making them indispensable in environments requiring extreme durability and load-bearing capacity, including offshore structures, pressure vessels, and heavy machinery.

Major applications for steel plates span across critical sectors, including the construction of bridges, commercial and residential buildings, oil and gas pipelines, and large-scale industrial equipment. The key benefit derived from using steel plates is their longevity and resilience to harsh operating conditions, coupled with their ability to be tailored to specific strength and corrosion resistance requirements through precise alloying. The primary driving factors propelling this market forward include increasing government investment in public infrastructure, the recovery of the global shipbuilding industry spurred by international trade demands, and the accelerating construction of wind energy and solar power infrastructure requiring specialized structural steel plates.

The Steel Plate Market is positioned for stable expansion, underpinned by cyclical upswings in core industrial activities. Current business trends indicate a strong move toward high-performance steel grades, such as high-strength low-alloy (HSLA) steel, driven by sustainability goals and the need for lighter, yet stronger, structural components in transportation and energy sectors. Supply chain resilience, following recent global disruptions, is now a major focus for producers, emphasizing localized or regionalized manufacturing hubs to mitigate risk and improve delivery times. Furthermore, consolidation among major steel producers is shaping the competitive landscape, focusing capital expenditure on technological upgrades for energy efficiency and reduced carbon emissions.

Regionally, Asia Pacific continues to dominate the market due to massive infrastructure projects in China and India, alongside sustained shipbuilding activities in South Korea and Japan. Europe is characterized by stringent environmental regulations, pushing the demand for green steel and specialized plates for offshore wind farms and complex engineering projects. Segment trends reveal that the shipbuilding segment remains a critical volume driver, while the growth rate of plates used in the oil and gas sector is experiencing stabilization, shifting focus towards maintenance and replacement rather than solely new exploration. The most rapid growth is observed in the heat-treated plate segment, catering to demanding applications like aerospace and high-pressure storage tanks.

Users frequently inquire about AI's potential to revolutionize material quality inspection, optimize complex rolling processes, and enhance demand forecasting within the volatile Steel Plate Market. Key themes revolve around how AI and machine learning (ML) algorithms can be integrated into steel production lines to achieve 'zero-defect' manufacturing and significantly reduce operational costs associated with energy consumption and scrap generation. Concerns often center on the initial investment costs for implementing sophisticated sensor networks and ML platforms, alongside the requisite upskilling of the workforce. Expectations are high regarding AI's ability to precisely predict fluctuations in raw material costs (iron ore, coal) and adjust production schedules dynamically to match real-time construction and manufacturing timelines, thereby providing a substantial competitive advantage to early adopters in supply chain management.

The dynamics of the Steel Plate Market are shaped by a complex interplay of internal market forces and macroeconomic factors. The primary drivers include massive global infrastructure spending, particularly in emerging economies focused on developing foundational transport and energy networks, alongside the increasing military shipbuilding requirements spurred by geopolitical tensions. However, this growth is significantly restrained by the high capital intensity required for steel manufacturing, coupled with global regulatory pressures related to carbon emissions, forcing producers to undertake costly green transition measures. Opportunities arise primarily from the expanding renewable energy sector, which demands vast quantities of specialized, corrosion-resistant, high-strength plates for wind turbine foundations and solar tracking systems, as well as the adoption of advanced manufacturing techniques like smart factories and digitalization.

Impact forces currently influencing the market include the fluctuating prices of essential raw materials (iron ore, coking coal), which directly affect profitability and pricing stability. Furthermore, trade protectionism, characterized by tariffs and quotas imposed by various countries, disrupts established global supply chains and forces companies to re-evaluate their export strategies. The overarching imperative of decarbonization serves as a powerful structural force, compelling the industry to invest heavily in low-carbon steel production methods (e.g., hydrogen-based reduction) that will fundamentally alter cost structures and production landscapes in the long term. These forces collectively determine the speed of innovation, investment decisions, and the geographical distribution of market share.

The Steel Plate Market is meticulously segmented based on product type, application, thickness, and end-use industry to reflect the diverse structural and functional requirements of its users. This segmentation provides crucial insights into targeted market development and resource allocation strategies. The primary segmentation revolves around metallurgical composition, differentiating between carbon, alloy, and stainless steel plates, where carbon steel plate holds the largest volume share due to its wide applicability in construction and general manufacturing, while alloy and stainless steel plates capture higher value due to specialized performance characteristics like corrosion and heat resistance.

Further analysis of the application segments, particularly focusing on shipbuilding and construction, reveals distinct demand cycles and quality requirements. Shipbuilding requires large volumes of high-weldability and fatigue-resistant plates, whereas construction projects necessitate robust structural integrity and adherence to regional building codes. The thickness segmentation is critical as it dictates the end-use, with plates below 50mm dominating general engineering and those above 100mm reserved for heavy engineering applications such as nuclear pressure vessels and heavy machinery components. Understanding these segmentation nuances is key for manufacturers to align their production capabilities with specific market needs and optimize their high-value product portfolio.

The value chain for the Steel Plate Market begins with the upstream sourcing of critical raw materials, primarily iron ore, coking coal, and ferroalloys, followed by energy-intensive steelmaking processes utilizing either Basic Oxygen Furnace (BOF) or Electric Arc Furnace (EAF) technologies. The efficiency and environmental compliance of these upstream operations dictate a significant portion of the final product cost. Key activities within the value chain include crude steel production, continuous casting into slabs, and finally, hot rolling and subsequent heat treatment (quenching and tempering) to produce the desired mechanical properties in the final steel plate product. Effective management of scrap steel input (especially for EAF producers) is crucial for both cost control and meeting sustainability metrics.

The downstream analysis focuses on processing, distribution, and end-user consumption. Steel plates are often distributed through a combination of direct sales from mills to large end-users (e.g., major shipyards or infrastructure contractors) and indirect sales via extensive distribution channels, including service centers and regional stocking distributors. Service centers play a pivotal role in the downstream segment by offering value-added services such as cutting, profiling, and surface treatment, tailoring the standard plate product to precise customer specifications. The final stage involves the utilization of the plates in fabrication processes for large structures, emphasizing the quality and traceability requirements demanded by certification bodies in sectors like oil and gas, and construction.

Potential customers for steel plates are overwhelmingly large-scale industrial consumers and fabrication specialists whose core operations depend on durable and high-strength structural materials. The primary buyers are entities involved in major capital projects requiring extensive steel infrastructure. These include global shipbuilding companies responsible for constructing container ships, tankers, and LNG carriers; engineering, procurement, and construction (EPC) firms managing large civil infrastructure projects like bridges, dams, and ports; and major industrial equipment manufacturers specializing in mining machinery, excavators, and heavy transportation assets.

Furthermore, the energy sector represents a critical customer base, encompassing companies building and maintaining oil and gas pipelines, storage tanks, and, increasingly, developers of renewable energy projects. Offshore wind farm constructors require enormous quantities of specialized thick steel plates for monopile foundations, while pressure vessel manufacturers require certified, heat-treated plates for boilers and chemical reactors. These customers prioritize material certification, consistent mechanical properties, timely delivery, and compliance with strict regulatory standards (e.g., API, ASTM, and specific maritime standards), often entering into long-term supply contracts directly with major steel mills.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 85.5 Billion |

| Market Forecast in 2033 | USD 118.8 Billion |

| Growth Rate | 4.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | ArcelorMittal, POSCO, Nippon Steel Corporation, China Baowu Steel Group, JFE Holdings, Tata Steel, Hyundai Steel, Essar Steel, thyssenkrupp AG, SSAB, JSW Steel, Ansteel Group Corporation, EVRAZ plc, TISCO, U.S. Steel Corporation, Gerdau S.A., Nucor Corporation, Commercial Metals Company (CMC), Emirates Steel, Outokumpu. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Steel Plate Market is rapidly evolving, driven by the dual goals of enhancing product performance and achieving drastic reductions in carbon emissions. The foundational technology remains the hot rolling process, but modern mills are now integrating Accelerated Cooling (AC) and Thermo-Mechanical Controlled Process (TMCP) technologies. TMCP is particularly vital as it allows producers to achieve superior strength, toughness, and weldability without relying heavily on expensive alloying elements, thereby enabling the production of advanced High-Strength Low-Alloy (HSLA) plates demanded by complex structural applications like bridges and pipelines.

The shift towards sustainable steel production represents the most significant technological disruption. Traditional methods are increasingly being replaced or augmented by Electric Arc Furnaces (EAFs), which utilize higher amounts of recycled scrap steel, resulting in a lower carbon footprint compared to Basic Oxygen Furnaces (BOFs). Furthermore, the industry is heavily investing in pilot projects for hydrogen-based direct reduced iron (H-DRI) technology, which aims to replace coking coal entirely in the reduction phase, offering a pathway toward near-zero emissions steel. Digitalization, often referred to as Steel Industry 4.0, involves deploying advanced sensor technology, big data analytics, and Artificial Intelligence (AI) across the rolling mill floor to optimize yield, minimize material waste, and ensure real-time quality assurance.

The APAC region holds the dominant share in the global Steel Plate Market, primarily fueled by the economic behemoths of China and India, alongside robust contributions from Southeast Asian nations. China remains the world's largest producer and consumer, driven by continuous, large-scale public and private infrastructure investments, including high-speed rail networks, urban development, and extensive bridge construction projects. Furthermore, South Korea and Japan maintain leading positions in high-value segments, particularly in specialized shipbuilding (LNG carriers, advanced naval vessels) and high-specification structural steel for seismic-resistant construction. The region's sustained growth is closely tied to rapid urbanization and industrialization, although environmental regulations in major economies are increasingly pushing for the adoption of higher-grade and more environmentally friendly steel production methods.

Infrastructure modernization programs, such as China's Belt and Road Initiative, create enormous, enduring demand for steel plates used in port expansion and cross-border energy pipelines. India’s focus on boosting domestic manufacturing through initiatives like 'Make in India' is accelerating the demand for industrial-grade steel plates for machinery, power generation components, and domestic defense shipbuilding. However, regional market stability is often subject to global trade disputes and overcapacity concerns, which occasionally pressure pricing and profitability. Despite these challenges, the sheer volume of consumption required to maintain the region’s development trajectory ensures APAC's long-term market leadership.

North America, encompassing the U.S., Canada, and Mexico, represents a mature but technologically sophisticated steel plate market characterized by high demand for quality, certified products, particularly in the energy and defense sectors. Growth in this region is significantly stimulated by government infrastructure spending, notably in the U.S., focusing on modernizing aging civil structures, bridges, and transport pipelines. The region exhibits a strong preference for domestically produced steel, often driven by 'Buy American' clauses and favorable governmental procurement policies designed to support national steel producers and ensure supply chain security for critical applications.

The primary growth drivers include the ongoing resurgence in oil and gas infrastructure replacement and expansion, requiring high-pressure line pipe steels, and the manufacturing sector's demand for high-strength steels for heavy machinery and mining equipment. Furthermore, the region is a leader in adopting EAF technology, placing it strategically for future low-carbon steel production, minimizing regulatory risk, and appealing to corporate customers with stringent sustainability targets. Investments focus heavily on digitalization (Industry 4.0) to maximize operational efficiency and reduce energy costs, ensuring North American producers remain competitive despite higher labor and energy costs relative to APAC.

The European Steel Plate Market is defined by stringent environmental standards and a pioneering push towards decarbonization, heavily influencing the technology and product mix. Demand is strong for high-performance and specialty steel plates used in advanced manufacturing, particularly in the automotive tooling, heavy engineering, and renewable energy sectors. Europe is the global epicenter for offshore wind energy development, necessitating vast quantities of specialized, ultra-thick, corrosion-resistant plates for turbine foundations and substructures. This niche but high-value segment provides significant revenue opportunities for European mills specializing in customized products.

The regulatory environment, including the EU Emissions Trading System (ETS) and proposed Carbon Border Adjustment Mechanisms (CBAM), accelerates the transition towards 'green steel' production technologies like H-DRI. While this transition involves considerable capital expenditure, it positions European producers as leaders in the sustainable steel movement, creating a competitive advantage when supplying environmentally conscious end-users. Demand also benefits from consistent investment in national rail and road networks, though market expansion is moderated by slower GDP growth compared to Asian counterparts. The emphasis on high quality, traceable steel remains paramount across critical end-use applications, ensuring premium pricing for certified European products.

The LATAM and MEA regions exhibit market growth tied closely to commodity price cycles and localized infrastructure requirements. In Latin America, countries like Brazil and Mexico drive demand, largely through oil and gas extraction projects, mining operations, and burgeoning construction sectors. Economic volatility and political instability occasionally restrain large-scale infrastructure investment, making the market highly sensitive to global commodity market fluctuations. However, significant potential lies in regional energy pipeline projects and modernization of port infrastructure to handle growing global trade volumes, which will require specialized structural and line pipe steels.

The Middle East and Africa (MEA) market is predominantly driven by massive state-led diversification and development programs, notably in the GCC states (Saudi Arabia, UAE). These projects include construction of smart cities, major transportation hubs, and large-scale industrial complexes (petrochemicals and desalination plants), requiring substantial volumes of steel plates, particularly corrosion-resistant grades due to the harsh coastal environments. The African market is characterized by slow but consistent growth related to energy infrastructure development and localized construction booms. Both regions benefit from strong demand for specialized plates for defense purposes and heavy oil & gas processing equipment.

The demand for HSLA steel plate is primarily driven by the need for materials that offer a superior strength-to-weight ratio. This allows for reduced material usage and overall structural weight, which is critical in sectors like transportation (lighter vehicles) and infrastructure (longer bridge spans, deeper offshore foundations) while maintaining or exceeding safety standards.

Decarbonization mandates are forcing steel producers to shift away from traditional coal-intensive processes (BOF) towards lower-emission technologies such as Electric Arc Furnaces (EAF), which utilize scrap steel, and the emerging pilot technology of hydrogen-based Direct Reduced Iron (H-DRI) to achieve substantial reductions in Scope 1 and 2 emissions.

The Construction and Infrastructure segment historically accounts for the largest consumption volume of steel plates. This includes extensive use in structural components for commercial buildings, industrial facilities, and major civil engineering projects like bridges, dams, and elevated highways, particularly in rapidly developing APAC nations.

Steel service centers are crucial middlemen in the downstream value chain, providing necessary value-added services such as precise cutting, profiling, thermal treatment, and inventory management. They bridge the gap between large steel mills and smaller end-users who require customized, just-in-time delivery of processed steel plate components.

The market outlook for steel plates in offshore wind energy is exceptionally positive. The rapid expansion of global offshore wind capacity requires large volumes of highly specialized, ultra-thick, corrosion-resistant steel plates for monopiles, jackets, and floating foundations, representing one of the fastest-growing niche application areas in the market.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.